The start of a new year is the perfect time to reflect on what you want to improve in your life and to create plans to make it happen. There is a good chance that you’re already thinking about resolutions like going to the gym more, eating healthier and volunteering with local organizations.

But what about financial resolutions? The beginning of the year offers the opportunity to focus on what’s going on with your money. With the right plan in place, you can stick to your financial resolutions and end the coming year in a better place than you started it.

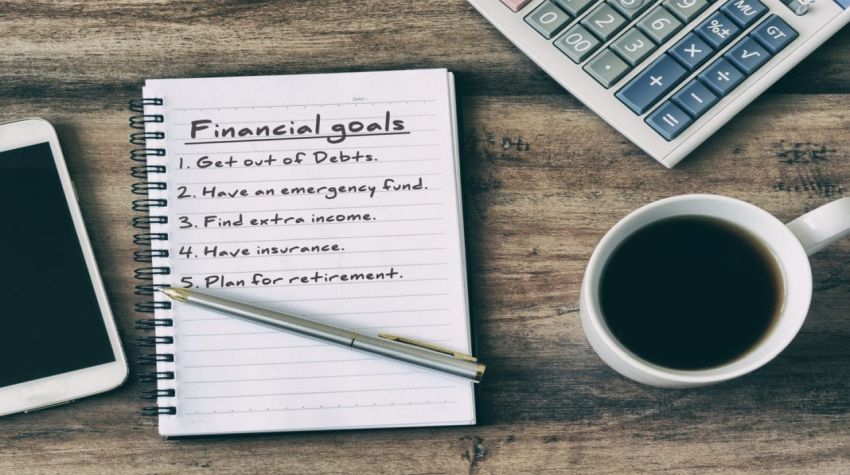

Bottom line: think about what you want from life in the coming year (and in the future) and set resolutions that can help you make the most of your financial resources. Remember that these goals are designed to help you live your life better, however, don’t forget to spend some time enjoying the here and now as well.